Smoke & Mirrors

2024 deluded us all. As macro headwinds continue, here's your 2026 playbook 📚

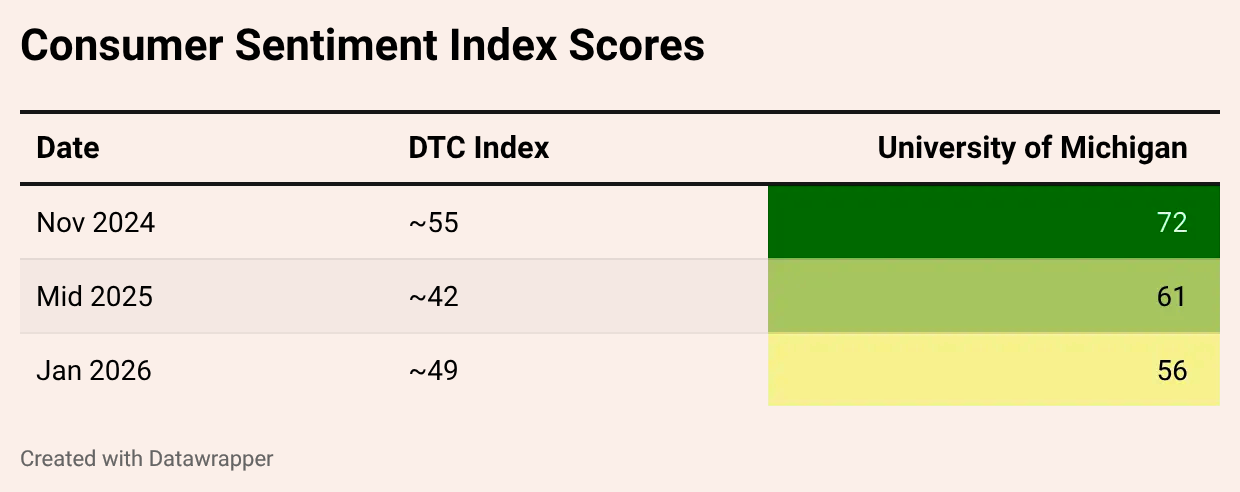

Consumer Sentiment

Looking at Consumer Sentiment Indices (CSI) from DTC Index (Common Thread Co & KnoCommerce) and University of Michigan, 2024 was a “recovery” year.

DTC Index’s CSI is a composite of three behavioral signals: past purchases, future intent, and economic feelings.

University of Michigan’s CSI is built on phone survey opinions.

The partial recovery from 42 to 49 is not a green light. Consumer willingness to spend is expected to remain below pre-2024 “recovery” levels through mid-2026.

Agora’s Verdict: Signal 🎯

Multiple Consumer Sentiment Indices confirm that the general population’s outlook on the economy has worsened. The Yotpo DTC Index, while relatively new and measuring performance of major, publicly traded DTC brands, also showed slight declines from 2025 to 2026.

Forecast

2025 underperformed both 2023 & 2024 on future purchase intent (next 3 months) and past purchase sentiment (last 30 days) according to DTC Index.

Notable:

The post-holiday spending pullback was deeper in 2025 than in 2023 or 2024.

Overall spending was down in 2025 compared to 2023 & 2024.

Actionable:

Plan for weaker revenue in March and April 2026.

Slight residual carryover from peak-holiday season, but normalizing.

Q4 2025 was a spike. Do not use it as a baseline for 2026 planning.

Depending on your annualized data, consider adjusting the following:

Inventory orders

Marketing spend

Cash flow planning

Agora’s Verdict: Signal 🎯

The US was never truly able to fix the underlying cracks in the economy. It’s nearly impossible to do so. Government stimulus made it so that no one could pin a “recession” on any one administration. It’s even harder to say whether we should have had a proper recession or if we’re long overdue for one.

Since 1945, recessions have occurred every 6.5 years on average. The Great Recession lasted 18 months. Most recently, the COVID contraction lasted just 2. The range of outcomes is wide, and the pressure underneath the current cycle has not been released.

Zooming Out & In

When looking back at the last three years, the data illustrates the following:

2023 — Deeply pessimistic across the board

2024 — Recovery year

2025 — Trend reverses

Notable:

Diving deeper into sentiment by age shows us:

Younger consumers are feeling the pinch on their wallets the hardest.

Older consumers, while sharing similar feelings about the economy, are generally better positioned to weather the storm.

Middle aged are…well somewhere in the middle on both sentiment and financial wellbeing.

Splitting by gender reveals:

Men are fairly neutral in their outlook on the economy.

Women are significantly more pessimistic.

Actionable:

Older men are the most resilient demographic in terms of demand.

Any other demographic will require fine tuning your messaging to ensure value and why now is the time to buy, are communicated clearly.

Agora’s Verdict: Mixed 😐

While age and gender are useful attributes in curating your messaging, economic outlook doesn’t necessarily correlate with one’s own volition when shopping.

Category Breakdown

Clothing & Fashion is the most resilient category. Buyers are above average on economic outlook and they drove the strongest holiday spend. Future purchase intent appears stable.

Food & Beverage — Viewed as necessary spending which is harder to cut. Brands not running subscriptions should start playing defense.

Health & Beauty — Similar to F&B, but less stable. Consumers are not as willing to buy at full price and are hungry for discounts.

Home & Garden — Swung down sharply after the holiday season.

Toys & Games — The poster child for discretionary “fun” spending that consumers are cutting. Prepare for an extended down cycle. This pullback is not cyclical.

Notable:

Clothing & Fashion requires a strong sense of brand identity to maintain defensibility.

Toys & Games has the lowest rate of self-identified “savers,” which might imply free-spending consumers. The reality is that casual players have exited entirely, leaving only the core spenders to carry the category.

The broader principle across all categories: Q4 is not a crutch that will carry you through the new year. Any brand without a strong value proposition beyond entertainment is exposed.

Actionable:

Look for ways to hook into broader, cultural moments. This goes beyond offering a Memorial or Labor Day discount. Search for non-traditional peak moments that you can speak passionately to (e.g. APL owning International Women's Day or Born Primitive leveraging D-Day). This gives you control over your own narrative and puts you into an echelon of your own.

APL made their International Women’s Day offer valid in-store, incentivizing loyal customers to come in and further cement their allegiance. It was an all-out media blitz with multiple articles not just praising women, but giving them a voice online on a variety of topics.

Born Primitive released a limited edition shoe & collector’s edition in commemoration of D-Day’s 80th anniversary. A portion of the proceeds were donated to veteran focused foundations. Collector’s edition bundles included ammo cans with engraved serial numbers, actual sand from Omaha Beach and Veteran baseball cards that highlighted individuals from D-Day during WWII.

Agora’s Verdict: Signal 🎯

Years of inflation and other economic events are being felt across the board. Tighten your ship and ensure that every dollar going out is getting put to good use. Riding the same waves as everyone else will make you more susceptible to economic shifts at home & abroad. Play defense and find a way to escape the crowded holiday discount frenzies.

Silver Lining for Non-Amazon Brands

Amazon’s share of DTC consumer spend has dropped from 2023 to 2025, while brand specific sites have picked up steam. Younger consumers are leaning towards brand-specific sites in a positive tailwind for Shopify and other DTC brands.

Notable:

Amazon is no longer the preference for young adults. This cohort has significantly shifted toward brand sites for their online shopping.

Clothing & Fashion brands are benefitting the most from this changing of the guards.

Home & Garden still dominates on Amazon.

Agora’s Verdict: Noise 🙉

Amazon still has a loyal base of shoppers amongst middle-aged and older folks. Their shopping experience still stands out as favorable to buyers who want to compare multiple brands quickly. The removal of the de minimis exemption tilts the playing field back in favor of higher priced products. This has profound effects on a marketplace like Amazon where Chinese brands had gained majority market share and were increasingly eating into other brands’ profits.

Fun Time’s Over

The “why” behind purchases has shifted significantly over the past three years.

Notable:

Problem solving as purchase motivation skyrocketed from 2023 to 2025. In 2026, it started to plateau. Still a major driver of purchases, consumers are looking to order products they view as a “need”.

Amongst 8 purchase drivers, “Highly Rated”, “Variety”, “Recommended” and “Makes Me Happy” are the most likely to trigger a purchase at checkout.

A new signal has emerged. “Like-minded community” has seen a noticeable uptick from 2023 to 2025 as a purchase motivator. Clothing & Fashion and Food & Beverage are best positioned to take advantage of this lever.

Actionable:

Prioritize messaging that highlights purpose, results or social belonging. Rational purchases don’t have to be dull. Put yourself in the shoes of the customer and ask yourself “what tangible value will I get from this?”. People are also naturally inclined to be part of a larger movement.

Nail down your product’s practical distinction.

Nutrition > junk food

Functional accessories > silly trinkets

Study Peloton’s community building tactics. Go beyond a loyalty program that does the bare minimum in signaling to customers that you just want them to spend more with your brand.

Agora’s Verdict: Signal 🎯

Consumer psychology doesn’t always translate to them clicking “Pay now”. However, the broader shift in the air reinforces the general theme here. How can you communicate that your product is worth buying right now?

The Spark

Purchase drivers come after a motivation leads the customer to search for a product and enter your orbit. Of the 8 purchase drivers mentioned above, very few are directly related to price.

Notable:

Price drivers are not the primary trigger for DTC consumers. However, “Low price” as a purchase trigger did see a slight increase in 2025.

Triggers by demographic:

Seniors depend more on ratings and value.

Women purchase mostly based on recommendations.

Men, like younger consumers, give more weight to happiness.

Amazon’s edge was highlighted above. This goes hand in hand with consumers who lean more on price and ratings as purchase drivers. Those consumers strongly prefer to shop on Amazon. Where DTC shines is with shoppers who make more emotion-based purchasing decisions.

Actionable:

Reviews and ratings are a defense against “Amazon drain”. Prioritize these as they’re top drivers of online purchases.

Invest in affiliate, UGC and influencers to ensure you have a recommendation loop to feed into the purchase triggers your brand is able to capitalize on.

Resist the urge to compete solely on price. This can backfire and push customers to Amazon. Not all customers want to be shopping there.

Agora’s Verdict: Signal 🎯

Purchase motivations and triggers allow for deeper analysis and clearer stories to be told about shoppers and their preferences. It goes beyond age, gender and the obvious stink around the economy.

Balling on a Budget

Consumers are increasingly self-identifying as a “saver” rather than a “spender”. From 2023 to 2025, this has accelerated to the point where the vast majority of shoppers are keeping a tighter grip on their wallets.

Notable:

Home & Garden consumers identifying as “savers” peaked in 2025, beating out consumers in other categories. This trend completely reversed at the start of 2026, as Home & Garden now has the most “spenders” amongst the pack.

The story is flipping for Clothing & Fashion shoppers. Consumers steadily shifted from a position of saving to spending, from 2023 to early 2026.

The overwhelming majority of shoppers still claim to be bargain hunters.

Health & Beauty saw the biggest decrease in consumer willingness to pay full price.

Toys & Games shoppers offer a more nuanced tale. They have the least amount of “savers”, yet their consumers are not necessarily looser with their spending habits. Enthusiasts in this category carry the spending patterns, while the casual consumer hangs back.

Actionable:

Prices are justifiable for the right product. Refine your messaging to reflect lasting value before resorting to price drops.

This doesn’t mean lazily applying “luxury” or “premium” verbiage and expecting customers to get it. These angles require more work to effectively show customers what they’re getting in exchange for a higher price.

Revisit your bundles and loyalty programs before jumping to discounts.

Agora’s Verdict: Mixed 😐

There’s some helpful context here on a category level. Not much is new in the grand scheme of things. Your brand has likely already seen some of these shifts play out thus far. The only verticals seeing sharp changes in consumer behavior from 2025 to 2026 are: Home & Garden and Health & Beauty.

The Revolution Will Not Be Televised

Social ads have surpassed TV as the leading channel for brand discovery. This shift became noticeable in 2024 and is here to stay.

Notable:

Social, TV and organic are the top performing discovery channels.

Influencer marketing saw a slight uptick from 2023 to 2025. This channel is especially prominent in Q4 when people are searching for gift ideas.

Podcasts have maintained stability in their corner of the Internet, with a small, but sizable chunk of the market.

Magazine & Radio are fading to black with barely any share of the discovery pie, along with Newsletters.

Organic (e.g. search, word of mouth) is holding its own despite paid social’s dominance.

Actionable:

Use the above “map” to reallocate your media spend accordingly. If you’re over-allocated in a weaker channel, adjust your budgets to reflect the current landscape for the rest of 2026.

If TV is in your media budget or will be in the future, it has its place alongside existing channels for broader awareness.

Supercharge your holiday sales with influencers in Q4 for more targeted marketing.

Reduce overreliance on any one channel.

Agora’s Verdict: Signal 🎯

For brands with a well-defined media strategy, this will help you continue to steer the ship as we reach the midpoint of 2026. If you’re still crafting a plan, you now have a starting point instead of trial by fire. Spending your hard-earned money is easy. Stretching each dollar and maximizing the return is what separates the winners from the losers.

The Social Network

YouTube is king. It dominates across every age and gender segment and is #1 for all of them.

Notable:

YouTube is strongest with men and teenagers, holding majority viewership amongst those groups.

Facebook usage amongst younger users continues to be on a steady decline.

Instagram has carved out a stable piece of the market. It performs best amongst early to middle aged adults and women.

TikTok lost a bit of their share, but is still a top platform for teens and young adults.

Pinterest is on a downswing towards irrelevance, while WhatsApp climbs the charts. Both hold negligible shares of the market.

Actionable:

A layered strategy works best. YouTube is your pillar as it reaches all ages.

Consider additional channels depending on your targeted age ranges.

TikTok for young adults and teenagers.

Instagram & Facebook for a trifecta covering adults up until middle age.

Facebook for the older, more senior crowd.

Agora’s Verdict: Signal 🎯

This takes the previous exposé further. Your brand does not need to be in all places at once. Hone in on where your audience spends their time and meet them there.

This article is not a substitute for the full data report provided by DTC Index.

I highly encourage you to purchase a subscription here.